In Part one of our Estate Planning blog, we discussed that every estate plan is unique and has many integrated parts. An estate plan usually includes a Will, Power of Attorney and a Representation Agreement. This blog discusses how tax planning is also an important part of a good estate plan.

Death and Taxes

When we discuss estate planning with our clients, the first thing many of them tell us is that they wish that all of their assets should be transferred to their family members. Unfortunately, they have not factored in that the Canada Revenue Agency will take their share first. This is because the Income Tax Act treats all of your assets as if they were sold at fair market value immediately prior to death even though there is no actual sale. These assets include shares of private and public companies, real estate and RRSP/RRIF accounts. The value of these assets can be significant which could result in a large tax liability at a tax rate of approximately 50%. Without the proper planning, the estate could be forced to sell some of the assets in order to fund the tax bill. Fortunately, by planning in advance, you can determine how to fund this tax liability and possibly defer it.

Tax Planning Options

i. After Death – Spousal Rollover: When you pass away, the Income Tax Act permits a transfer of your assets at cost to your spouse or a testamentary spousal trust through a concept referred to as a spousal rollover. As a result of a spousal rollover, the tax on your RRSP/RRIF and on any accrued capital gains will be delayed until the earlier of the sale of the assets or the death of your spouse.

ii. While you are Alive – Joint Spousal Trust: An effective way to set up a spousal rollover during your lifetime is to establish a joint partner trust. In our second blog, we discussed that joint spousal trusts are one way to plan for probate. We will discuss the use of trusts further in part 3 of our Estate Planning blog.

iii. Corporate Family Planning: As mentioned above, if you own shares of a private corporation, you will be subject to tax at the time of your death if there is an accrued gain on the value of your shares. One planning technique to lock in your gain and predetermine your tax liability, while at the same time possibly defer the tax on the future growth of the shares, is by implementing an estate freeze.

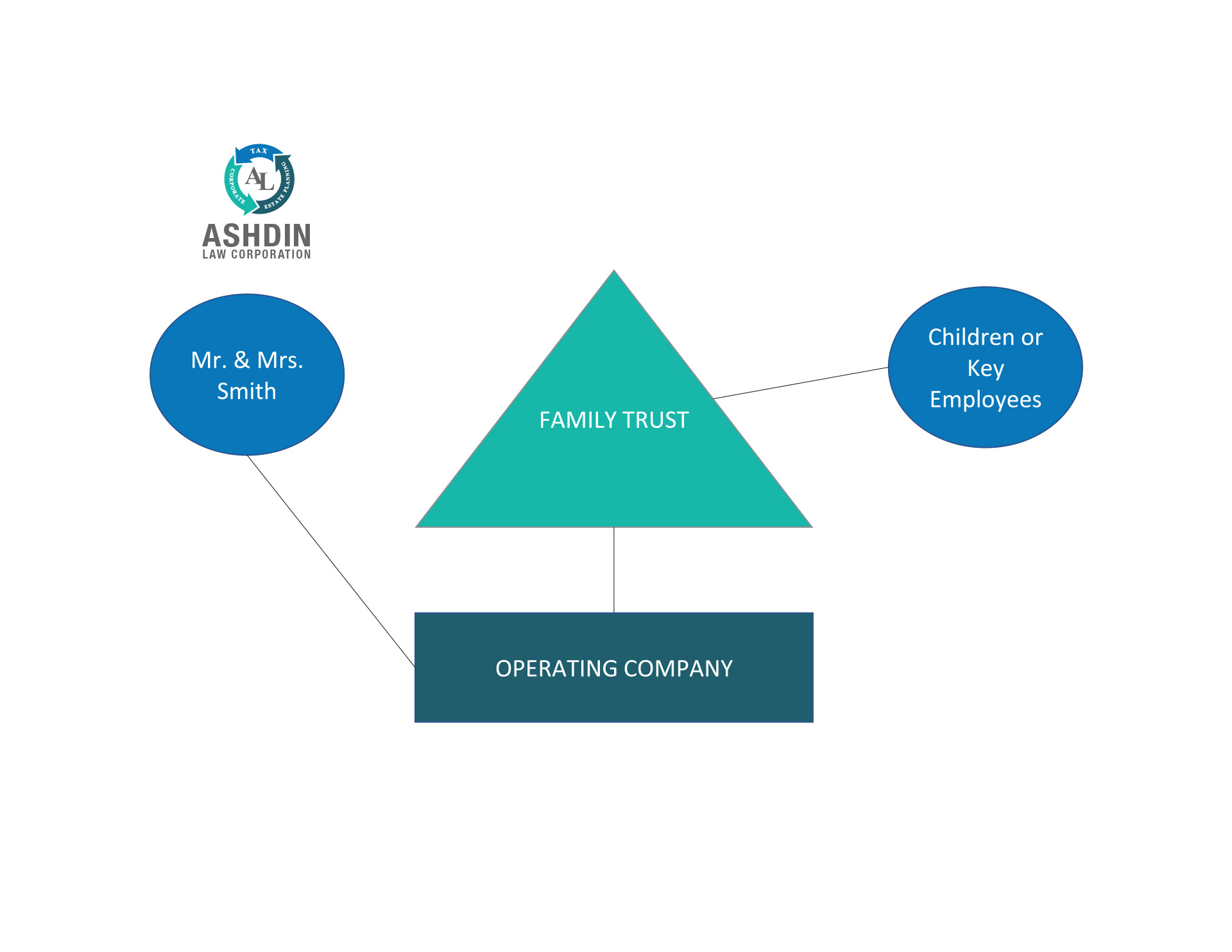

What is an Estate Freeze?

An estate freeze is the term commonly given to a transaction where you lock in or “freeze” the value of your shares of a private small business corporation. In simple terms, an estate freeze is accomplished when a taxpayer exchanges their shares at cost for fixed value, redeemable & retractable preferred shares equal to the fair market value of the company at that point in time. Because the shares are exchanged at cost, no gain is triggered and there is no immediate tax liability as a result of the exchange of shares. Further, since the value of the preferred shares is fixed, we can calculate the amount of tax that will be payable in the future when the taxpayer passes away. The taxpayer can then plan on how they will fund this tax liability during their lifetime. At the same time, new shareholders can subscribe for new common shares of the company at a nominal value. If drafted properly, all future growth of the company will be attributed to these new shares.

An estate freeze is best described through an example:

Mr. and Mrs. Smith are each 66 years old and each own 100 common shares of Smith Enterprises Ltd. which have a cost of $10 each. The fair market value of the company is $2,000,000. Mr. and Mrs. Smith have two children that are a part of the business and would like to take it over one day as they would like to continue to grow the business. Mr. and Mrs. Smith would like to transfer ownership of their business to their children without triggering an immediate tax liability and are mindful that their children do not have $2,000,000 to buy them out. Therefore, Mr. and Mrs. Smith decide to complete an estate freeze by exchanging their common shares of their company for fixed value redeemable and retractable preferred shares worth $1,000,000 each. The value of the company at this moment in time is attributed completely to the preferred shares. The Smith’s children could then subscribe for new common shares of Smith Enterprises Ltd. at a nominal value. Alternatively, Mr. and Mrs. Smith could settle a family trust that includes their children as beneficiaries. This family trust could subscribe for new common shares of Smith Enterprises Ltd. as well. All future growth of Smith Enterprises Ltd. after the estate freeze is completed will be attributed to the new shares. Further, the Smith’s have locked in their future tax liability as it relates to the $2,000,000 value of their preferred shares.

The benefits of an estate freeze are:

- Facilitates succession planning – As the example above demonstrates, an estate freeze allows new shareholders, the Smith’s children, to take over the business at a nominal cost.

- Tax Deferral – the tax on the future growth of Smith Enterprises Ltd. will now be payable when the Smith’s children sell their shares rather than when the Smith’s pass away.

- Multiplication of the lifetime capital gains exemption – A benefit of using a family trust is that it may be possible to multiply the benefit of the capital gains exemption to all of the individual beneficiaries of the trust. In 2019, the lifetime exemption is equal to approximately $866,000 per individual.

- Potential Source of retirement income at a lower tax rate – As noted above, the Smith’s will receive fixed value, preferred shares as a part of an estate freeze. These shares may be sold back to the company by the Smith’s over time to provide a source of income during retirement. This income will be taxed at the Smith’s marginal tax rates which should be less than the highest marginal tax rate that will likely apply in the year of death.

- Funding of tax liability on death – As discussed above, the Smith’s have locked in their future tax liability as it relates to the $2,000,000 value of their preferred shares. If the Smith’s do not redeem their preferred shares during their lifetime, an effective and practical way to fund this tax liability is to purchase life insurance.

If you would like to learn more about tax planning considerations for your estate plan you can connect with Ish Lila or Shelly Lila at Ashdin Law – Corporate and Tax Lawyers, located in Coquitlam, B.C.

The above provides a practical overview about tax planning considerations for your estate plan. This blog is for informational purposes only. Readers are cautioned this blog does not constitute legal or professional advice and should not be relied on as such. Rather, readers should obtain specific legal advice in relation to the issues they are facing.